Investing Analysis

What Are The Main Strategies?

When discussing the main strategies of investing there are multiple options. We can help you figure out which strategy works best for you and your investment.

Calculators

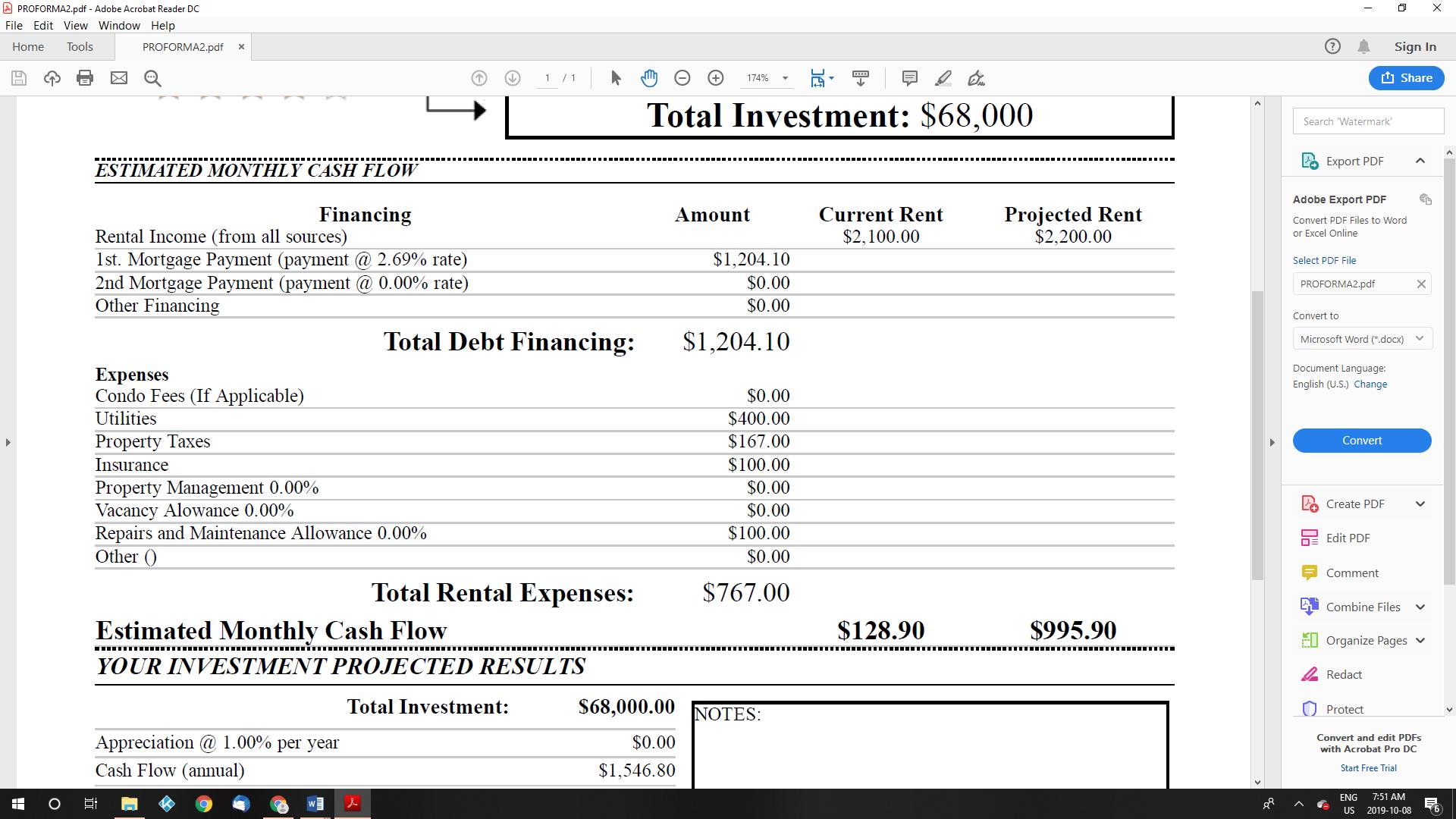

There are many different formats and types of rental property calculators. The calculators help a property owner or manager determine the rate of return, the cap rate and the cash flow on your property. Remember there are 3 ways to make a profit in holding a rental property in your investment portfolio:

- Positive cash flow paid each month

- Mortgage Pay down

- Increase in Value

The most conservative way to look at the rate of return is to implement a similar program to what a banker would look at when evaluating your investment property for financing.

Banks are normally the most risk adverse group so if we use the same numbers as the bank, we will be reducing our risk, but also understanding if we will have any issues qualifying for the financing.

The inputs we use are, Rental income, projected rental income, acquisition costs, renovations costs required to get the property ready to rent, property expenses, vacancy rate and management fees. You can increase your rate of return by managing the property yourself or doing some of the repairs yourself.

I have found that people either love having rental properties or they hate it. For me, over the years I have had some challenging properties and some challenging situations.

However, I have usually made a profit and the rates of return have been very good for me. The rental property calculator, works by inputting all of the variables such as the property’s purchase price, the mortgage amount and rate, loan term and expected monthly rent. It also includes how much you put for a down payment, renovation costs, and any acquisition costs including lawyer fees, inspections and appraisals. After entering these numbers, the rental income calculator will calculate your cash flow, your cap rate and your return on investment.

Purchase Price

The purchase price will be an estimate of what you think you can negotiate for the property. It is important to have a professionals help you with the purchase. Getting a home inspection will ensure that you are not missing the age of the roof or furnace and helps to understand what the issues are before you purchase. Once you have all of your projected costs you will be able to come up with the total investment needed.

Next Steps

The next step is to determine what your financing costs will be. As an investor in a rental property, most major banks will require you to put down at least 20 percent of the purchase price as your down-payment. If you are planning to live in the property, you may be able to put down as little as 5 percent. This will allow you to get started as a landlord and begin your portfolio.

It is important to remember that in Canada you will require someone to insure your mortgage if you are putting down less than 20 percent. There are a few different mortgage insurance companies in Canada, with the biggest being CMHC (Canadian Mortgage and Housing Company) and Genworth.

The insurance rates can be as high as 4.6 percent so when you are putting down a 5 percent down payment, almost all of it will be taken by the insurance company. Don’t worry, the bank will give you the money by adding it to your mortgage. After all, who wouldn’t want to lend money if it was insured? When I bought my first property I put down 10 percent.

I was working two jobs, at the Canadian Imperial Bank of Commerce and at Canada Safeway at nights and on weekends. After being there for a short time, I put in a basement suite. It only cost me $10,000 in 1993, and I rented it out for $800 per month. It was just over one year to pay back that investment.

Fixed or Variable Rate?

When you are looking for your financing you should look at all of the options to see where you can get the best rate. One of the main questions that people ask is should I go with a variable or fixed mortgage rate. It is always an interesting discussion where we go over the past 25 years rates and see that the variable has seemed to be a lower rate, we then look at the term, a 3 year or 5 year, which is best? I think it comes down to a few variables that you need to decide when making your decision about financing.

1) Do you want to be looking at the interest rates all of the time with a variable mortgage

2) What is the cost of having a 5 year locked in rate

If you are comfortable knowing that you will probably pay a bit more for a 5 year locked in term mortgage, but you will know what your costs are and be able to sleep better at night, then I would suggest that you go with the 5 year guaranteed rate.

If you like to analyze the markets and try and predict the ups and downs and think you can time it well, then you probably can save some money by going with a shorter term or a variable mortgage. It is usually a trade-off between comfort and knowing the costs verses speculating and spending the time to educate yourself to time your mortgages.

As you get more properties, you should consider spreading out your mortgages and renewal dates so that they are not all coming due at the same time. I think that is a good way to spread out the interest rate risk.

Interest rates have fluctuated from 21 percent to the current lows of today. You can choose to ride the variable rate roller coaster or lock in for a five year fixed. Choose what is best for your rental business.

{kind=link}

{kind=link}

{kind=link}

Expenses

A great way to increase your profit is to manage expenses well. Obviously a big part of the expense in the first few years will be your interest. As you continue to pay this down, you will be making more profit every year. Some of the other big expenses are repairs, property management, and vacancy. It is critical to keep your properties rented.

In bad times you should be lowering your rents and in good times you should be increasing them. Avoiding an empty month will be one of the best ways you can keep your profits high. For example, if your monthly rent is $2400 and you lose one month’s rent, you could have lowered your rent by $200 a month and at the end of the 12 month lease, you would have been in the same position.